Last month, CHIRblog released a trove of investigative reports and case files from the U.S. Department of Labor (DOL) relating to multiple employer welfare arrangements (MEWAs), including association health plans (AHPs). We’ve been diving deeper into these records since then, and wanted to share some takeaways about common types of misconduct that DOL has documented.

Self-dealing and other prohibited transactions are rampant

DOL’s case reports are rife with examples of AHPs and other MEWAs engaging in self-dealing—that is, the association or individuals in positions of responsibility taking action to benefit themselves, rather than plan participants and beneficiaries—or other similarly problematic behavior.

A common scenario involves an association, either directly or through a wholly owned subsidiary, receiving fees for administrative or marketing services it purports to provide to the plan it sponsors. Although such arrangements are not always illegal, associations can engage in unlawful self-dealing when they or their subsidiaries charge the plan more than they directly spend to provide services or simply accept payments for services that aren’t performed. This is because plan fiduciaries—those with “discretionary control or authority over plan assets or administration”—are required to “run the plan solely in the interests of participants and beneficiaries” and “may not engage in transactions on behalf of the plan that benefit parties related to the plan, such as other fiduciaries, service providers, or the plan sponsors.”

Here are just a few, recent examples of this type of conduct from DOL’s files:

| Case No. |

Description |

| 70-016407 | California Trucking Association improperly collected nearly $300,000 in marketing and administrative fees and commission payments from the fully insured AHP it sponsored between 2010 and 2013, because it was a plan fiduciary and this constituted self-dealing. |

| 43-009439 | ICUL Service Corporation (ServiceCorp), a for-profit, wholly owned subsidiary of the Indiana Credit Union League, collected $1,841,249 in commissions from insurers marketing the Indiana Credit Union League’s plans between 2010 and 2013. DOL determined that ServiceCorp overcharged the plan by $572,420 during this window, taking in more than 1.45 times what it could document spending. |

| 43-008516 | Two wholly owned subsidiaries of Ohio Bankers League together collected a total of $4,367,117 in administrative fees and commissions from January 1, 2010 to April 30, 2016, but they could only document direct expenses of $2,690,693. The remainder, $1,676,425, was considered excess payments and thus improper under ERISA. |

It also appears relatively common for associations to use plan assets for improper purposes, such as expensive travel and meetings, and to make excessive or otherwise unjustified payments to external parties. One example is Case No. 72-033685, in which DOL found that the United Agricultural Employee Welfare Benefit Plan & Trust had paid millions of dollars in marketing, travel, and meeting expenses between 2007 and 2014 that were not reasonable or incurred for the exclusive benefit of plan participants and beneficiaries. Another is Case No. 72-033881, in which DOL found that hundreds of thousands of dollars were inappropriately transferred from the plan to its sponsor, the National Association of Prevailing Wage Contractors, Inc. (NAPWC), and that the plan had also made millions of dollars of improper and excessive payments to other parties, including the plan’s broker and attorneys. And, in at least two cases (Case Nos. 22-013388 and 71-010061), DOL found that associations were improperly using plan assets to pay lobbying and legal fees to advance their interests before state legislative and regulatory authorities.

Stepping back, what’s notable in these and other cases is that this type of misconduct isn’t limited to “fly-by-night” self-funded AHPs that collect premiums but then disband leaving millions of unpaid claims. It also happens with otherwise legitimate AHPs offering fully insured health plans that are staying on top of claims. But participating employers and employees are still getting cheated, paying extra to line the pockets of association executives.

Actuarial Analyses Are Often Unused or Ignored

When hundreds of thousands or millions of dollars in claims go unpaid, it is common for DOL to find that the individuals running the plan failed to conduct due diligence in setting rates and otherwise take basic steps to maintain the financial health of a plan.

This frequently means that the plan sponsor or administrators never consulted an actuary when setting up a self-insured plan. In at least some of these cases, the plan sponsors or administrators simply adopted the rates and benefits that they or another entity had been using or relied on an insurance agent’s recommendation, and hope for the best. The investigation into the Sommet Group Employee Benefit Plan, Case No. 40-021633 is a good example of this. As DOL observed in its quarterly report, “Sommet did not hire an actuary to set the premium amounts for the new self‐insured arrangement. Sommet took the BCBS benefit booklet and the premium amounts and used those for the new Plan. . . . Sommet wanted employees to have the exact same coverage and at the same amount.” This did not work out, however: after a little over two years, Sommett had collected $8.8 million in contributions but owed $10 million in claims.

In other cases, the quarterly reports show that an actuary was retained, but their recommendations were ignored. One example of this is Case No. 22-014423, which was the second investigation into the Pennsylvania Builder Association in just a few years. The first investigation, Case No. 22-013388 (referenced above) found $12 million in prohibited transactions related to the association’s operation of a fully insured plan. Near the end of this investigation, which culminated September 2008, the association switched to a self-insured plan. Unfortunately, by December 31, 2009, this new plan had accumulated nearly $6.4 million in unpaid claims and was insolvent. The plan actuary told DOL that he had “repeatedly informed the trustees . . . that the Plan could not be maintained at the current pricing,” but his advice apparently went unheeded.

As highlighted in a few examples below, plans’ rate-setting failures are often compounded by a failure to acquire appropriate stop-loss insurance to help manage risk.

Case No. 30-103258 (New Jersey Tool and Manufacturers Association) |

Case No. 40-018695 (Georgia Plumbers Trade Association Health Plan) |

Case No. 30-100312 (New Jersey Licensed Beverage Association Employee Benefit Plan) |

As these and other cases show, absent proper actuarial guidance, a plan can become insolvent and face millions of dollars in unpaid claims very quickly. Self-insured MEWAs are required to disclose whether they have stop-loss insurance on their Form M-1, and, when noticed, the absence of stop-loss insurance can trigger an investigation by DOL. See, e.g., Case No. 40-18732. But there is no express assurance that a plan has taken the basic and critical step of consulting a licensed actuary in setting rates.

{kind=link}

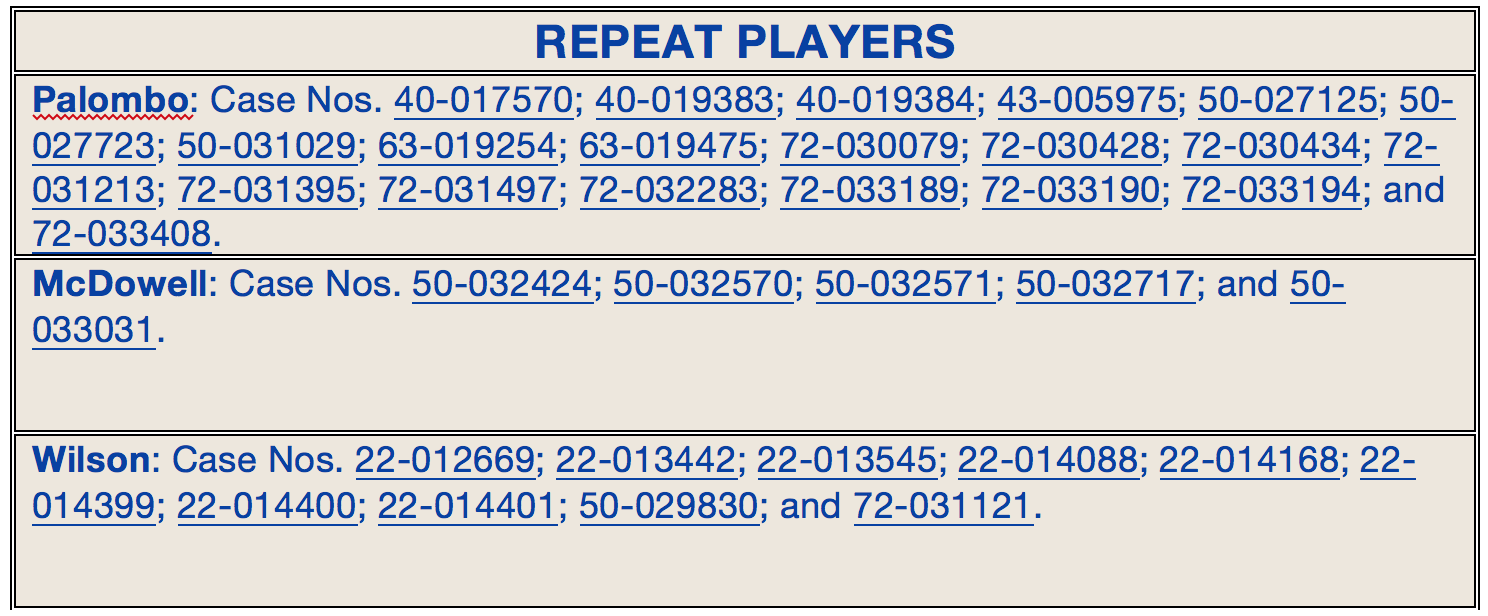

| REPEAT PLAYERS |

| Palombo: Case Nos. 40-017570; 40-019383; 40-019384; 43-005975; 50-027125; 50-027723; 50-031029; 63-019254; 63-019475; 72-030079; 72-030428; 72-030434; 72-031213; 72-031395; 72-031497; 72-032283; 72-033189; 72-033190; 72-033194; and 72-033408. |

| McDowell: Case Nos. 50-032424; 50-032570; 50-032571; 50-032717; and 50-033031. |

| Wilson: Case Nos. 22-012669; 22-013442; 22-013545; 22-014088; 22-014168; 22-014399; 22-014400; 22-014401; 50-029830; and 72-031121. |

Repeat Players, Repeat Harm

Although they make up a relatively small proportion of the total number of individuals and entities involved in running AHPs and other MEWAs, the quarterly reports include several repeat players who have caused outsized harm across both time and geographic regions.

One particularly egregious example is the series of interconnected cases involving the Progressive Health Alliance (PHA) and its successor association, the Contractors & Merchants Association (CMA). PHA and CMA were purported employer associations run by Raymond Palombo. According to the quarterly reports and related investigative files, from 2002 until at least December 2010, Palombo placed members of PHA and then CMA into a series of union-sponsored health plans that apparently made a practice of accepting new groups of participants from other defunct MEWAs and/or purported Taft-Hartley health plans (that is, health plans established pursuant to collective bargaining agreements between unions and employers). Although these plans were often originally established as legitimate Taft-Hartley plans, DOL determined that they lost this status once they began accepting more participants like those in PHA who were not subject to collective bargaining agreements. Sometimes these placements lasted for only a few months at a time before Palombo moved them to a new plan, leaving millions of dollars of unpaid claims in their wake. Notably, DOL found that many of the union-sponsored plans that Palombo turned to, as well as various third-party administrators and brokers his associations and the plans contracted with, were run by many of the same people—often, family members or former colleagues of Palombo or others involved in the arrangements.

A similar scheme occurred beginning in 2010involving the Master Contract Group Bargaining Association (MCGBA), later to be known as the American Workers Master Contract Group, an employer association formed by Herb McDowell. Like with the other scheme, DOL found that MCGBA would contract to have its clients participate in a series of union-sponsored plans, but they never engaged in collective bargaining. Rather, as DOL put it in Case No. 50-033031, “[i]t appears that the employers signed up through the MCG and ‘joined’ [the union] simply for access to the union’s health benefits.” It is likewise apparent that the association did not exist for any purpose other than providing employers from unrelated industries access to lower-cost health insurance. Unlike the other line of cases, this one did not appear to result in major unpaid claims, but it did involve significant self-dealing and other prohibited transactions, as McDowell and his relatives also operated several third-party service providers and other businesses with various ties to the associations and plans. Indeed, based on documentation it reviewed, DOL estimated that the affiliated parties and service providers involved in this arrangement received approximately $5.2 million in compensation from January 1, 2010 through June 20, 2014. McDowell, and companies owned by him, received $1.58 million of this. For participating employers, including the Lutheran Church, these fees altogether resulted in an undisclosed markup of approx. 15-30% from their base premiums.

A third broad-reaching scheme involved Ron Wilson who, through various entities including R.J. Wilson & Associates, Inc. (Case No. 22-014401), Medical Benefit Administrators of Maryland, Inc. (Case No. 22-014400), and Dayspring Management LLC (Case No. 22-014399), marketed and administered MEWAs, including multiple AHPs, that he described as “fully insured under ERISA.” This labeling confused state regulators, and misled prospective and participating employer groups and participants about the type of protection they would be getting. In DOL’s view, these plans were self-insured arrangements, with stop-loss insurance provided by Lloyd’s of London, an offshore insurance company. What’s more, DOL found that several of Wilson’s MEWAs each faced hundreds of thousands of dollars of unpaid claims because Wilson and his affiliate companies failed to charge employers sufficient premiums, despite the ability to raise rates every six months, and failed to make claims on the off-shore Lloyd’s policies. More generally, Wilson’s scheme highlights the frequently problematic role that off-shore insurers and other financial institutions play with respect to AHPs and other types of MEWAs, as these entities are not subject to any state or federal regulation and can more readily escape judicial enforcement. For other examples of schemes involving off-shore insurers, see Case Nos. 40-016947, 40-017635, 40-021635, 43-006667, 50-026032.

DOL’s primary response to more egregious misconduct is to seek permanent injunctions barring the individuals involved from acting as fiduciaries to or otherwise providing services related to employee benefit plans. This may be effective in the majority of cases, but it is apparent from the quarterly reports that at least a small number of individuals are unswayed by such orders (and the threat of being held in contempt for violating such orders) and/or rely on family members to continue acting in their stead. Absent more effective tools to prospectively screen who can act as a plan fiduciary, these bad actors can continue to cause outsized harm to employers, employees, and others they come into contact with along the way.

Next week, we will delve further into federal enforcement efforts to protect the public from fraudulent and poorly managed MEWAs, and the effectiveness of these efforts. Stay tuned!