There’s an emerging media narrative that the Affordable Care Act (ACA) marketplaces have stabilized, with premium increases moderating, some new market entrants, and existing insurers expanding their service areas. This narrative suggests that critics of the Trump administration’s ACA policy decisions were overly pessimistic about their effects.

However, our review of insurers’ regulatory filings for proposed 2020 premiums paints a far less rosy picture than the surface-level reports about premium trends.

The bottom line for 2020 is that premiums will be far higher than they should be, and many insurers are gloomy about long term enrollment and health status trends in the ACA-compliant market.

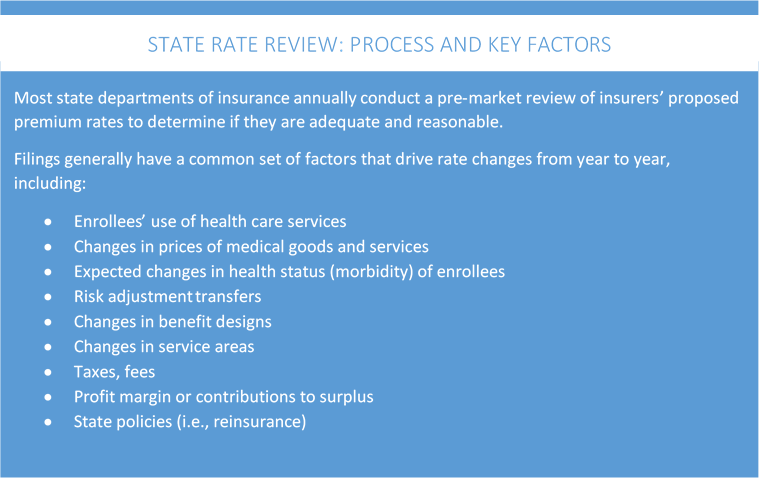

Five states – Maryland, New Mexico, Oregon, Vermont, Washington – and the District of Columbia (D.C.) publish these filings in late May or early June (most other states will receive rate filings later in June or July). We reviewed the actuarial memos from a sampling of insurers in all six jurisdictions; where a state has only two insurers participating we reviewed filings from both. Most insurers in these states predict that, over time, the ACA market will become smaller and sicker, largely due to repeal of the ACA’s individual mandate and other Trump administration policy decisions. At the same time, many of these same insurers are seeking modest average increases or even decreases for their 2020 premium rates. See Table.

Table. Average 2020 Proposed Individual Market Rates in States with Early Filing Deadlines

| State | Average Proposed Rate Change | Number of Insurers |

| DC | 9.0% | Two |

| Maryland | 2.9% | Two |

| New Mexico* | N/A | Six |

| New York** | 8.4% | Thirteen |

| Oregon | 3.3% | Seven |

| Vermont | 12.5%*** | Two |

| Washington | 0.96% | Thirteen |

*No average rate change available

**New York has published insurers’ 2020 rate requests but not the underlying filings

***Non-weighted average

Most ACA Insurers Increased Premium Rates Too High in 2018

Do you remember 2017? In January of that year, the President issued an executive order committing to undo the ACA. The Republican-led Congress spent nine months on repeal and replace efforts. Over the spring and summer the Trump administration threatened to – and ultimately did – cut off the ACA’s subsidies that reduce cost-sharing for lower income marketplace enrollees (insurers’ lawsuits to recoup losses from that decision are now before a federal appeals court). Most observers expected that the administration would not enforce the ACA’s individual mandate, and indeed, the penalty for failing to have coverage was eliminated in December of that year. The Trump administration also announced that they would expand the availability of alternative, underwritten products such as short-term plans that would siphon young and healthy people away from ACA-compliant products.

The result of all this policy activity? Massive market uncertainty and an expectation that many healthy people would abandon their ACA coverage. In response, insurers hiked their premiums for 2018, on average, 32 percent for silver plans and 19.1 percent for gold plans. They held these rates relatively steady for 2019, with an average 1.5 percent rate decrease. However, rates were still on average 6 percent higher than they would have been without the individual mandate repeal and the expansion of short-term health plans.

It’s now clear that many insurers raised premiums in 2018 more than was necessary. A Kaiser Family Foundation analysis of insurers’ 2018 financial data found that the loss ratios (the percentage of premium revenues spent on medical claims) of individual market insurers dropped to an average of 70 percent. Their average per member/per month (PMPM) margins increased to $166.82 (compared to an average PMPM loss of $9.21 in 2015). As a result, insurers expect to owe consumers $800 million in medical loss ratio rebates for 2018.

The 2020 rate filings we reviewed confirm that many insurers set premiums too high in 2018 and 2019. Those proposing rate decreases, such as Regence Blue Cross Blue Shield in Washington, point to 2018’s “favorable financial experience” as a factor. Or, as Molina puts it in its New Mexico filing: “[Our] 2018 claim cost experience is less adverse than that assumed in the current rates.” The rate decreases they are proposing are an effort to get closer to their actual claims costs (and avoid paying those big medical loss ratio rebates).

Insurers Predict that Individual Market Enrollment will Flatten or Decline, Become Sicker

Most insurers predict that their overall membership will remain the same or decline over time, and that those who leave the ACA-compliant individual market will be healthier on average than those who remain. CareFirst in D.C. reports a “deterioration” of their claims experience, while BridgeSpan in Washington writes: “The Individual market has contracted in recent years and that trend is expected to continue. This will lead to greater market-wide average morbidity as relatively healthier members opt to forego coverage.” Kaiser Permanente in Maryland has the same prediction, pointing primarily to the “elimination of the Individual Mandate.” The company expects fewer people than in past years will renew their plans, and that “terminating members are anticipated to have lower morbidity.” Conversely, Kaiser Permanente’s Washington actuaries expect their membership to “remain steady,” with no change in their overall health status.

Several Other Factors are Driving Proposed Rate Changes

In addition to the increased use of services among their enrollees, insurers cite several other factors driving premium rates higher. These include:

- The prices for medical goods and services, with specialty pharmaceuticals singled out as a primary source of higher costs (for BCBS of Vermont, this latter category is driving 7.9 percent of their total rate increase);

- The return of the ACA’s health insurer fee in 2020 (it was temporarily suspended for 2018); insurers in the above states expect it to add between 2-3 percent to premium costs.

- The expansion of association health plans (AHPs) (MVP of Vermont predicts that AHPs will result in a 1 percent increase in market-wide morbidity in 2020).

Notably absent from these early rate filings is any mention of the effect of the Trump administration’s policy encouraging the expansion of short-term health plans. This could be because all five of these states and D.C. have effectively nullified the federal standards by enacting state-level limits on the marketing of these products. Soon, filings will be posted in states that have not regulated short-term plans and a better sense of how they have impacted the ACA-compliant market may be available.

Also not mentioned in these rate filings was the Trump administration’s June 13 final rule encouraging the use of Health Reimbursement Arrangements (HRAs). If employers offer HRAs for 2020 in significant numbers, it’s likely to change the size and overall health status of the individual market (by 2029, the Trump administration predicts that 11.4 million people will be enrolled in individual insurance via an HRA). Some health plans may seek to revisit their 2020 projections now that this rule has been finalized.

What Can Shoppers for Health Insurance in 2020 Expect?

At least in these early filing states, consumers will see insurer participation in the ACA marketplaces stay stable; in some areas they may see more competition. But health insurance in the individual market remains too expensive (the average monthly cost of a high deductible bronze plan in 2019 is $339), particularly for those ineligible for the ACA’s premium subsidies. Modest rate increases or decreases in 2020 do not change that fact. The ACA marketplaces will continue to see declines in new enrollees without policy actions to improve coverage affordability, increase outreach to the uninsured, and discourage the growth of alternative products that can cherry pick young, healthy consumers.

2 Trackbacks and Pingbacks